Most Singaporeans have basic medical coverage, but neglect the importance of elevating our healthcare beyond the basics. Here's why Integrated Shield (IP) Plans are more important than you think.

For those of us who are still young and healthy, we probably do not pay too much attention to the cost of hospitalisation. This might be so especially in Singapore, where we are well covered under different insurance programs offered by the government, such as MediShield Life (MSHL).

But is that good enough?

Table of contents

- How Much Do Wards Actually Cost in Singapore?

- Integrated Shield Plans Complement MediShield Life

- Different Types of Integrated Shield Plans

- Deductibles and Co-Insurance

- How to Evaluate Different Integrated Shield Plans

How Much Do Wards Actually Cost in Singapore?

Ward costs comprise a huge chunk of hospitalization costs, with charges varying depending on the type of ward. Private wards are the most expensive, offering upgraded amenities and better privacy, while Ward Type C in public hospitals offers basic facilities with up to 8 beds per room.

Using Singapore General Hospital as an example, the following table compares the cost of different types of wards in a public hospital here in Singapore:

|

Type of wards |

Description |

Rate |

|

Private Ward |

|

|

|

Standard Ward Type A |

|

|

|

Standard Ward Type B1 |

|

|

|

Standard Ward Type B2 |

|

|

|

Standard Ward Type C |

|

|

Source: Singapore General Hospital and Pacific Prime Singapore

As you can see, although the wards of the lowest category start from SGD 37 per day, it only offers a basic room shared by 8 beds.

For something that is a bit more customised, for example, having the option to choose your own meal, the price would go up >7x to SGD 269 per day for B1 wards.

But more importantly, the government’s MSHL plans only cover the basic types of wards (C and B2). If you want anything more comfortable, you will either have to pay a hefty sum or you can plan ahead with additional insurance coverage such as Integrated Shield Plans (IPs).

Opting for additional coverage comes with its own benefits, as Class A and private hospital wards are superior to the basic wards covered under MediShield Life. In addition to better privacy, patients also gain access to better service, shorter waiting times, enhanced safety measures, and overnight family accommodation.

Integrated Shield Plans Complement MediShield Life

Integrated Shield Plans are medical insurance plans that offer additional benefits on top of those provided by MSHL.

As highlighted in the example above, while MSHL only covers wards of B2/C types in public hospitals, IPs can get a policyholder covered for B1/A wards, or even for some private hospitals. Besides better wards, IPs also cover pre- and post-hospitalization expenses.

Many benefits under IPs are offered on the basis of “as charged”, unlike MSHL’s benefits that are mostly capped at limits. If the charges go beyond these limits, the patient with only MSHL will still have to bear the additional cost, which is far from ideal in case of severe health issues.

The following table showcases the extent of coverage for select items under MSHL and Raffles’ Integrated Shield Plan:

| Item |

MediShield Life (Coverage up to/Capped at) |

Raffles’ Shield Plan |

|

Surgery |

SGD 240 – SGD 2,600 |

As charged |

|

Surgical Implants & Approved Medical Consumables |

SGD 7,000/Treatment |

As charged |

|

Accidental Inpatient Dental Treatment |

Not covered |

Covered |

|

Kidney Dialysis |

SGD 1,100 per month |

As charged |

|

Chemotherapy |

SGD 3,000 per month |

As charged |

Source: Raffles Health Insurance

Bottom line: MSHL’s coverage is decent but far from enough. Complementing MSHL with an IP offers much better coverage and protection.

Different Types of Integrated Shield Plans

Currently, the following private insurers in Singapore offer different types of IPs, targeting various categories of wards (above B2) in public and private hospitals:

- Income

- AIA

- Great Eastern

- Prudential

- SingLife

- HSBC Life

- Raffles Health Insurance

Since IPs are added onto the mandatory basic MSHL, their premiums are also usually quoted together with MSHL.

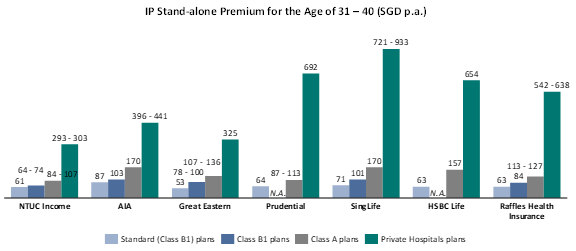

We’ve compiled the following chart comparing the stand-alone premium (i.e., excl. MSHL for the age of 31 - 40) of IPs offered by different providers:

The premium amount jumps significantly from class A IP plans to private hospital ones. Looking at the premium amount alone, Income seems to offer the most affordable IPs across different categories.

Other than premiums, you will also need to co-pay (deductibles and co-insurance) with the insurers in case medical expenses are incurred.

Looking for an affordable Integrated Shield Plan (IP)? Singlife Shield Starter* covers you with up to S$20,000 per policy year for hospital bills at just S$300 (before GST) fully payable by MediSave — great for young adults who want basic. For more coverage, add on the rider, Singlife Health Plus Starter, at just S$1 (before GST) and reduce co-payment of your hospital bills to just 5%!

*T&Cs apply. This product is underwritten by Singapore Life Ltd. SingSaver is not an insurance agent/intermediary and cannot solicit any insurance business, give advice, recommend any product or arrange any insurance contract. Please direct all enquiries to Singapore Life Ltd. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Deductibles and Co-Insurance

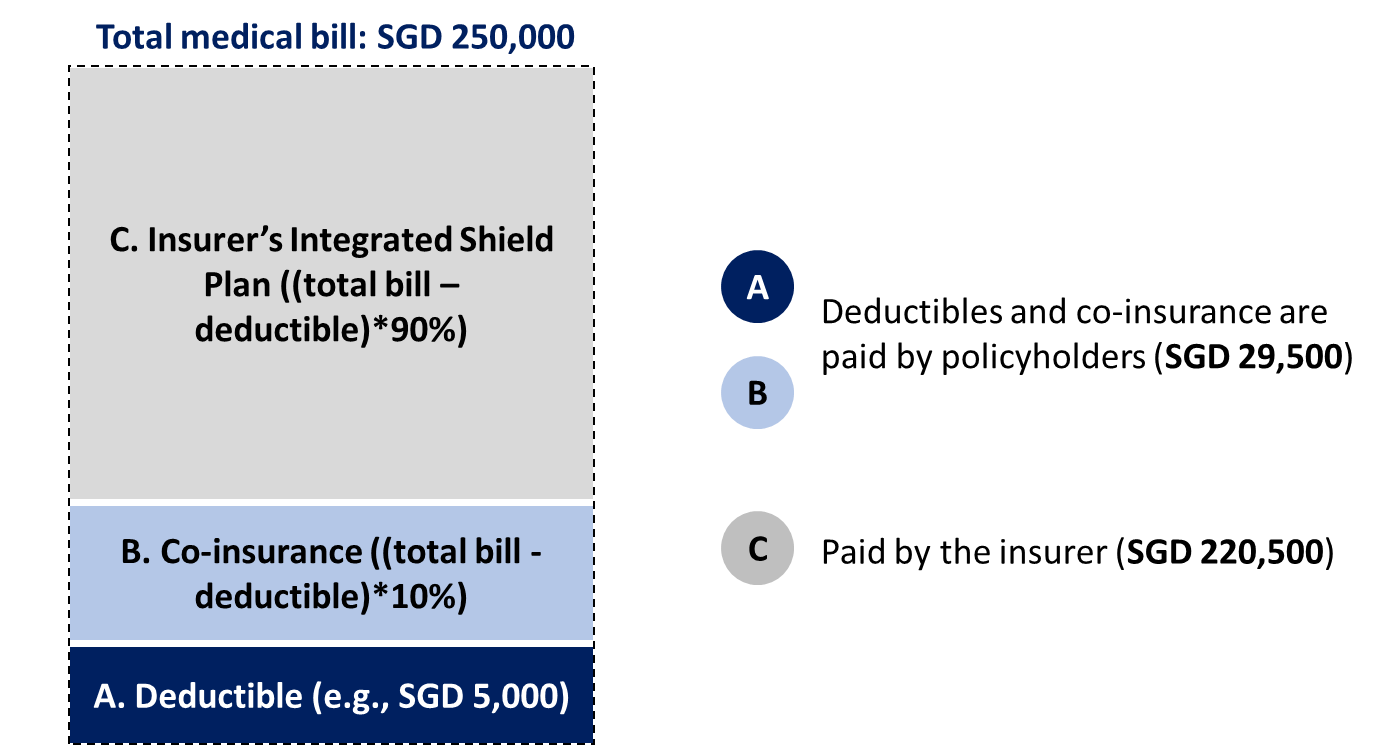

Deductibles and co-insurance are out-of-pocket expenses paid by the policyholders instead of the insurers.

A deductible is the initial amount you have to pay for medical claims made in a policy year before you can start receiving any payouts from the insurance policy.

Co-insurance is like splitting the medical bill with the insurer. For IPs, the co-insurance amount a policyholder has to pay is a fixed percentage (usually 10%) of the total bill after meeting the deductibles.

For example, if the total medical bill is SGD 250,000 and you have an IP plan with an annual deductible of SGD 5,000 and a 10% co-insurance feature, you will need to pay SGD 5,000 deductible and 10% of the remaining bill after deductible (i.e., SGD 250,000 – SGD 5,000).

In this case, your out-of-pocket expenses for the medical bill would be SGD 29,500 (5,000 + 10%*(250,000 –5,000)). The remaining portion would be paid out by the insurer.

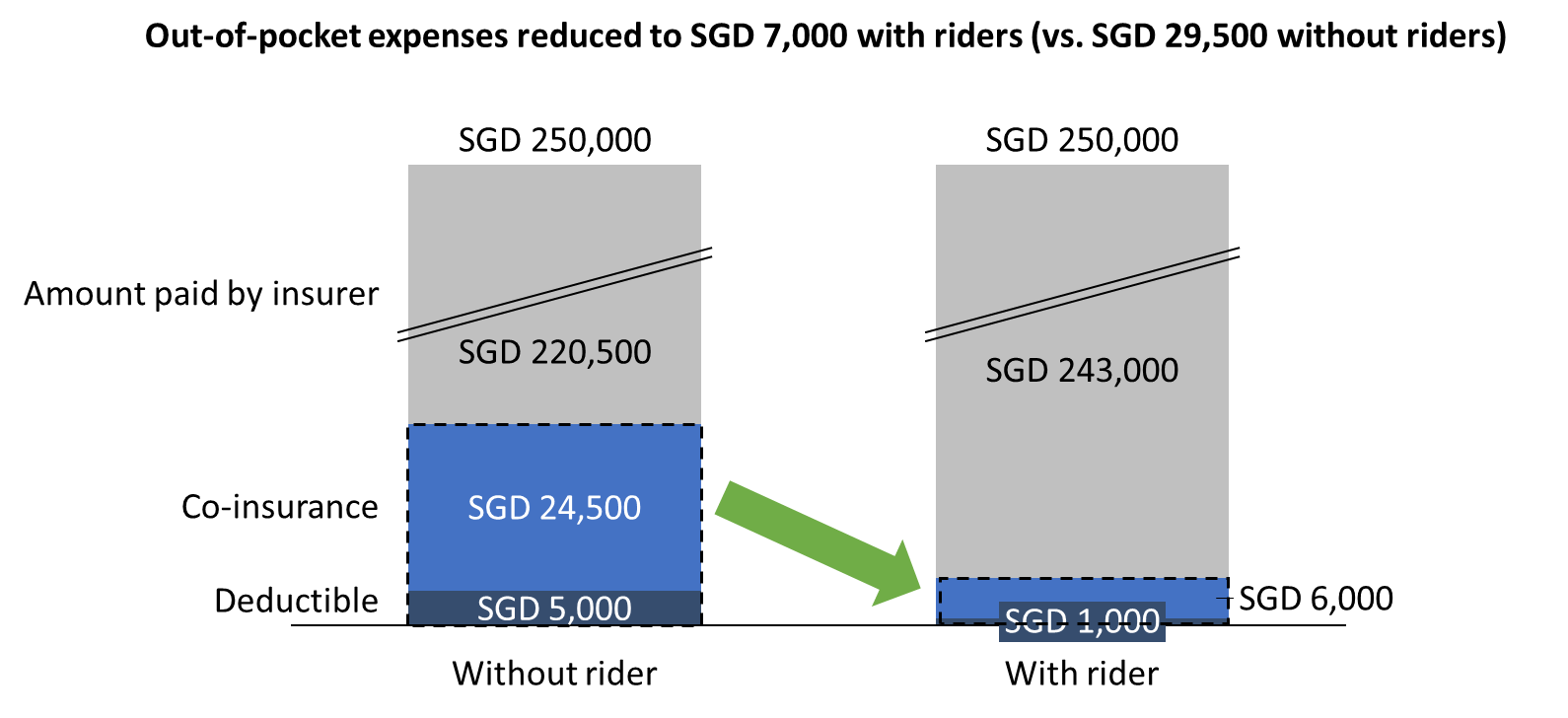

Riders that can further reduce your deductibles and cap your total co-insurance amount are also available in the market. You can add them to reduce your out-of-pocket expenses.

Using the example above and assuming that you add a rider that can reduce your deductible to SGD 1,000 with the co-insurance amount capped at SGD 6,000 per policy year, the following chart demonstrates how much you save:

How to Evaluate Different Integrated Shield Plans?

Premium or pricing is only one of the factors you should consider when evaluating different IPs. The reason certain IP policies are cheaper is usually due to less protection or coverage being offered.

After all, IPs’ additional protection and coverage is the main reason you are paying for them, instead of just going with the basic MSHL. So, it is important to choose the right IPs that fit your needs the most, rather than the cheapest ones.

Ask yourself these questions: are you okay with B1 wards instead of A wards? Do you only want private hospitals? The premium will only go up as you expect better wards and wider coverage.

It is easy to compare IPs based on different ward types, but it gets increasingly complicated and technical when looking at coverage for specific treatment/illness, where many conditions and restrictions may apply, as seen in the following table that compares select benefits across different IPs under the same category:

|

Class A plans |

Income |

AIA |

Great Eastern |

|

Select benefits |

Enhanced IncomeShield Advantage |

HealthShield Gold Max B |

GREAT SupremeHealth A PLUS |

|

Psychiatric |

|

|

|

|

Inpatient Palliative Care |

|

|

|

|

Cancer Drug Treatment |

|

|

|

|

Pre-Hospitalisation Treatment (no of days indicate max no of days covered prior to admission) |

|

|

|

|

Post-Hospitalisation Treatment (no of days indicate max no of days covered after discharge) |

|

|

|

To save time and get the best advice, talk to an insurance agent who specialises in these products. Alternatively, you can also compare the best Integrated Shield Plans right here on SingSaver!

Read these next:

Best Integrated Shield Plans in Singapore (2023)

The Difference Between MediSave And MediShield Life: A 2-minute Explainer

9 Things You Should Know About Your MediShield Life

Personal Accident vs Life & Medical Insurance: What You Need to Know

Best CareShield Life Supplement Plans In Singapore

Similar articles

Integrated Shield Plan Riders Now Require Co-payment: What You Need To Know

Why You May Not Want an A-class Ward (Even if Your Insurer is Paying)

What Does the Medishield 5 per cent Co-pay Really Fix?

Best Integrated Shield Plans in Singapore (2025)

3 Reasons Why Singaporeans Can’t Switch from Private to Subsidised Healthcare

Prudential PRUShield Integrated Shield Plan Review 2021: Multi-option IP with Something for Everyone

How Can I Get The Most Value Out Of My Integrated Shield Plans?

Is the B1 Health Insurance Plan in Singapore Worth It?

Back to Blog

Back to Blog