Singaporeans and PRs enjoy universal healthcare, but what does that actually mean?

Singapore is lauded for having one of the best healthcare systems in the world, but as with all things, quality comes at a cost.

It’s a good thing then that we have MediShield Life, which is a national healthcare insurance scheme to keep things affordable.

Here are nine things you should know about MediShield Life, so you can make an informed decision on how to make the best use of your policy.

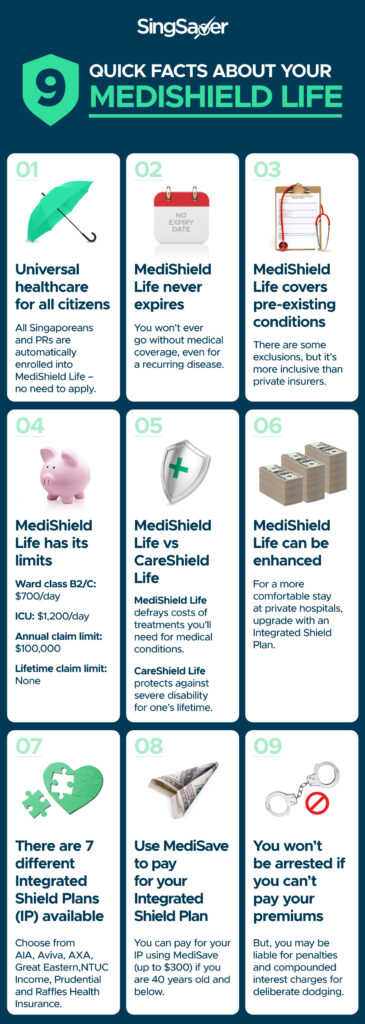

#1 MediShield Life offers universal healthcare for all citizens

Are you a Singaporean or a Permanent Resident? If so, then congrats — you’re automatically enrolled into MediShield Life. This means there’s no need for you to apply to join the scheme, and you may tap on your MediSave Account to help pay for medical treatments and procedures you may need.

Although touted as a universal healthcare plan, MediShield Life does not cover each and every health condition. In particular, procedures that are aesthetic or elective in nature (wisdom tooth surgery, for example), are not covered.

See Ministry of Health’s list of exclusions for more details.

#2 MediShield Life never expires

Unlike other private health insurance schemes, MediShield Life never expires. You won’t ever find yourself going without medical coverage, or prevented from making a claim for a recurring disease.

Which brings us to our next point.

#3 MediShield Life covers pre-existing conditions

Probably the best thing about MediShield Life is that it covers pre-existing conditions.

Private health insurers exclude pre-existing conditions, which can add to the stress of receiving a diagnosis for a serious disease if you’re completely uninsured. (Wow, brain cancer with no way to pay for its treatment? What spectacular luck!)

However, with MediShield Life, you are guaranteed to be covered for a portion of your medical bills, as long as your condition, treatment or procedure does not fall under the exclusion list.

This holds true even if you have an Integrated Shield Plan; you may lose the coverage by your private insurer, but will retain your MediShield coverage.

#4 MediShield Life has its limits

But that’s not to say that MediShield Life is without limit. Although you can claim for a wide range of healthcare needs, there are caps on each claim item. For example, you can claim up to S$700 per day for ward classes B2/C. This limit is increased to S$1,200 per day for intensive care wards.

Also, in aggregate, the annual claim limit per policy year is capped at S$100,000. But the good news is there is no lifetime limit.

Ministry of Health (MOH) has also just announced that from September 2022, patients will be able to claim up to S$9,600 per month for selected cancer drug treatments, as well as an additional S$1,200 for other services like blood tests, scans and medical consultations. Currently, eligible patients are only able to claim up to S$3,000 per month under MediShield Life coverage.

#5 MediShield Life vs Eldershield — What’s the difference?

Although MediShield Life and Eldershield are both healthcare insurance plans, they are meant to cover against different health risks.

MediShield Life is a general-purpose healthcare plan that focuses on helping you receive the treatment you need for various medical conditions.

Eldershield, on the other hand, focuses on protecting against severe disability. It is designed to provide financial assistance to individuals aged 40 onwards, who are saddled with disability issues that affect their mobility, and ability to feed and dress themselves.

Together, MediShield Life and Eldershield act as safety nets that cover acute conditions to long-term health issues.

(Note: Those with serious pre-existing illnesses have to pay an additional 30% premiums for the first 10 years. Also, later this year, ElderShield is set to be replaced by CareShield Life, an updated long-term disability insurance.)

#6 MediShield Life can be enhanced to provide better coverage

The benefits under MediShield Life is pegged to the costs of Class B2/C wards in government hospitals. So, do note that the MediShield Life payout will only make up a small proportion of the bill if you were to choose to stay in a Class A/B1 ward or in a private hospital.

If you prefer to have more coverage when pursuing treatment at private hospitals or want a higher-tier ward, you can do so through an Integrated Shield Plan (IP).

#7 There are 7 different Integrated Shield Plans available in Singapore

Integrated Shield Plans (IPs)are offered by private insurers, so you’ll have to go to them to purchase one. Here are the seven existing IP providers on the market:

- AIA

- Singlife

- AXA

- Great Eastern

- Income Insurance

- Prudential

- Raffles Health Insurance

#8 You can pay for your Integrated Shield Plan using your MediSave Account

As mentioned, IPs can come with more expensive premiums (VS Medishield Life). To help Singaporeans pay their IPs, an Additional Withdrawal Limit was introduced in Nov 2015.

This means you may now pay for your IP premiums using your MediSave Account, but only up to a cap. Any shortfall will have to be paid for out of pocket (with cash).

Here are the prevailing Additional Withdrawal Limits for purchase of IPs, sorted by age bands:

- S$300 for those with age next birthday 40 and below;

- S$600 for age next birthday 41 to 70; and

- S$900 for age next birthday 71 and above

#9 You won’t be arrested if you can’t pay your MediShield Life premiums

For the vast majority, MediShield Life premiums are automatically paid via their MediSave Account. The Government also offers targeted subsidies (up to 50%) to help ensure MediShield Life remains affordable for as many Singaporeans as possible.

However, what if for some reason or another, you are unable to afford your MediShield Life premiums? Well, you won’t be arrested for not being able to afford your premiums, so you can rest easy on that front.

Like any insurance scheme, MediShield Life only works properly if policyholders play their part. So if you have the means, pay up. At the very least, you’ll be doing your part to keep premiums manageable for everyone.

Besides, if you’re thinking of deliberately dodging your payments, know that you’re liable for penalties and compounded interest charges.

Read these next:

Best Integrated Shield Plans in Singapore (2020)

Personal Accident vs Life & Medical Insurance: What You Need to Know

Baby Insurance: What’s Worth Buying For Your Newborn?

5 Best Personal Accident Insurance Plans In Singapore (2020)

All The Insurance Terms And Lingo In Your Policy, Explained

Similar articles

Integrated Shield Plan Riders Now Require Co-payment: What You Need To Know

Why You May Not Want an A-class Ward (Even if Your Insurer is Paying)

Why Integrated Shield Plans Are Essential and How to Find the Right One for You?

MediShield Life Promises More Coverage and Benefits in 2021 – What Does This Mean For You?

What Does the Medishield 5 per cent Co-pay Really Fix?

Medi-Curious? Here’s Your Complete Guide To MediFund

What’s The Difference Between MediSave And MediShield Life: A 2-minute Explainer

Panel vs Non-panel Doctors: What’s The Difference, And Which Specialist Should You See?

Back to Blog

Back to Blog