For Singaporeans, CPF elicits a range of emotions, from curiosity to confusion.

You would be forgiven for thinking that Singapore's Central Provident Fund (CPF) is some sort of a mythical beast or an obscure deity, with all the constant chatter whenever the subject is broached.

Adding to the noise is the latest increase in salary ceiling from $6,000 to $8,000 by 2026 for CPF contributions after the Budget 2023 announcement.

While some may lament the lower take-home salary, when you take a longer lens, the change ultimately benefits most Singaporeans with a higher rate of savings for retirement income, housing, and medical needs.

Agreed, CPF is complicated, but that’s only because it is so tightly integrated into the fabric of Singapore’s economic and social tapestry. So, to help you make sense of it all, here’s our complete beginners’ guide to CPF in Singapore.

- What is CPF

- How do CPF contributions work?

- CPF contributions and allocations

- What is the CPF Annual Limit?

- The 4 CPF accounts and their uses

- The CPF interest rates

- Conclusion

Looking to grow your savings quicker? Consider a low-risk short-term endowment.

SingSaver Exclusive Offer: Open a CMC Invest account and receive S$20 cash via PayNow. Promo is stackable with CMC Welcome Offer. Valid till 1 May 2025. T&Cs apply.

What is CPF?

As mentioned earlier, CPF stands for Central Provident Fund. It's a compulsory, employment-based savings scheme.

Under the CPF scheme, all Singaporeans are required to make regular contributions to the Fund, which invests the proceeds on their behalf for their future benefit.

This works similarly to Malaysia's Employee Provident Fund (EPF), Hong Kong's MPF (Mandatory Provident Fund), and the USA's 401(k) programme. However, Singapore's CPF has a wider range of uses besides just retirement. This includes healthcare, education, and housing.

Each eligible Singaporean will have their own individual CPF account to which these contributions are deposited. Much like with a bank savings account, these deposits earn interest, allowing the CPF account holder or member to grow their money.

It is this accumulation of wealth that allows CPF to fulfil its intended function of helping Singaporeans meet their financial needs.

The CPF scheme is run by the Central Provident Fund Board (CPFB), although in common speak, ‘CPF’ is used to refer to both the scheme and the entity controlling it.

Only Singaporean Citizens and Singaporean Permanent Residents are eligible to join the CPF.

Money in one’s CPF account is not allowed to be withdrawn unless under special circumstances. These include a renouncement of citizenship if you migrate and being officially certified to have a reduced life expectancy.

.png?width=800&height=250&name=WeBull_7Apr-1May_INBLOGBANNER_800x250%20(1).png)

SingSaver Exclusive Offer: Open a Webull account and fund a minimum of USD 2,000 to receive S$125 Cash. Fund USD10,000 to get a Dyson SSHD 15 (worth S$649), an Apple AirPods Pro (Gen 2) with Magsafe Charging Case (worth S$349), S$320 cash, or S$320 Shopee Voucher. Promo is stackable with Webull Welcome Offer of free USD600 AAPL shares and more. Valid till 1 May 2025. T&Cs apply.

How do CPF contributions work?

Under the scheme, employees earning more than S$500 per month have to contribute a portion of their salary to their CPF account. The rates of contribution vary according to age bands, slowly reducing from age 55 onwards. However, this does not apply to individuals working overseas as CPF contributions aren't mandatory in that instance.

Do note that other payments attract CPF contributions as well. These include commissions, cash incentives, and bonuses.

Employee CPF contributions are matched by their employer, who has to make a separate contribution to the employee’s CPF account. The employer’s contribution rate varies according to the age of the employee.

Here’s a look at the present CPF contribution rates (from 1 January 2024):

| Age of employee | Contribution rates by employee (% of wages) | Contribution rates by employer (% of wages) | Total contribution as % of wages |

| 55 and below | 17 | 20 | 37 |

| Above 55 to 60 | 15 | 16 | 31 |

| Above 60 to 65 | 11.5 | 10.5 | 22 |

| Above 65 to 70 | 9 | 7.5 | 16.5 |

| Above 70 | 7.5 | 5 | 12.5 |

To illustrate how the contribution works, let’s use Mary, 26, as an example. She earns a gross wage of S$4,000 per month. Since she is aged under 55, her CPF contribution rates are as follows:

| Gross wage | S$4,000 |

| Mary’s take-home pay: 80% | 80% x S$4,000 = S$3,200 |

| Mary’s CPF contribution: 20% | 20% x S$4,000 = S$800 |

| Employer’s CPF contribution: 17% | 17% x S$4,000 = $680 |

| Total contribution to Mary’s CPF account = S$1,480 | |

Although Mary contributes only 20% of her gross salary, the amount contributed to her account exceeds the 20%. That’s because her employer has to contribute more to her CPF equal to 17% of her gross wage.

CPF contributions and allocations

Each CPF member starts off with three accounts — the Ordinary Account (OA), Special Account (SA), and Medisave Account (MA). They also gain a fourth account, the Retirement Account upon turning 55. We’ll detail out the differences between these four accounts, but for now, let’s get back to Mary’s allocation rate.

We know that her account receives a monthly contribution of S$1,480. This sum is split among her three accounts, OA, SA and MA, and the allocation ratios are as follows:

|

Age band |

Allocation ratio |

|

35 and below |

OA: 0.6217 SA: 0.1621 MA: 0.2162 |

|

Above 35 – 45 |

OA: 0.5677 SA: 0.1891 MA: 0.2432 |

|

Above 45 – 50 |

OA: 0.5136 SA: 0.2162 MA: 0.2702 |

|

Above 50 – 55 |

OA: 0.4055 SA: 0.3108 MA: 0.2837 |

|

Above 55 – 60 |

OA: 0.3872 SA: 0.2741 MA: 0.3387 |

|

Above 60 – 65 |

OA: 0.1592 SA: 0.3636 MA: 0.4772 |

|

Above 65 – 70 |

OA: 0.0607 SA: 0.303 MA: 0.6363 |

|

Above 70 |

OA: 0.08 SA: 0.08 MA: 0.84 |

Note that the allocation ratios are applied on the total CPF contribution for the month, (in Mary’s case, S$1,480).

The allocation rates among the three accounts change according to your age, in a move designed to help members better meet different needs at different life stages.

💡 According to the CPF, a larger percentage of your contributions are allocated to your OA when you're younger to support your first home purchase.

In short, the allocation ratios for your SA and MA gradually increase with age, while the allocation ratio for your OA gradually decreases. Also, from age 55 onwards, the contribution to your MA sharply rises.

CPF contribution caps

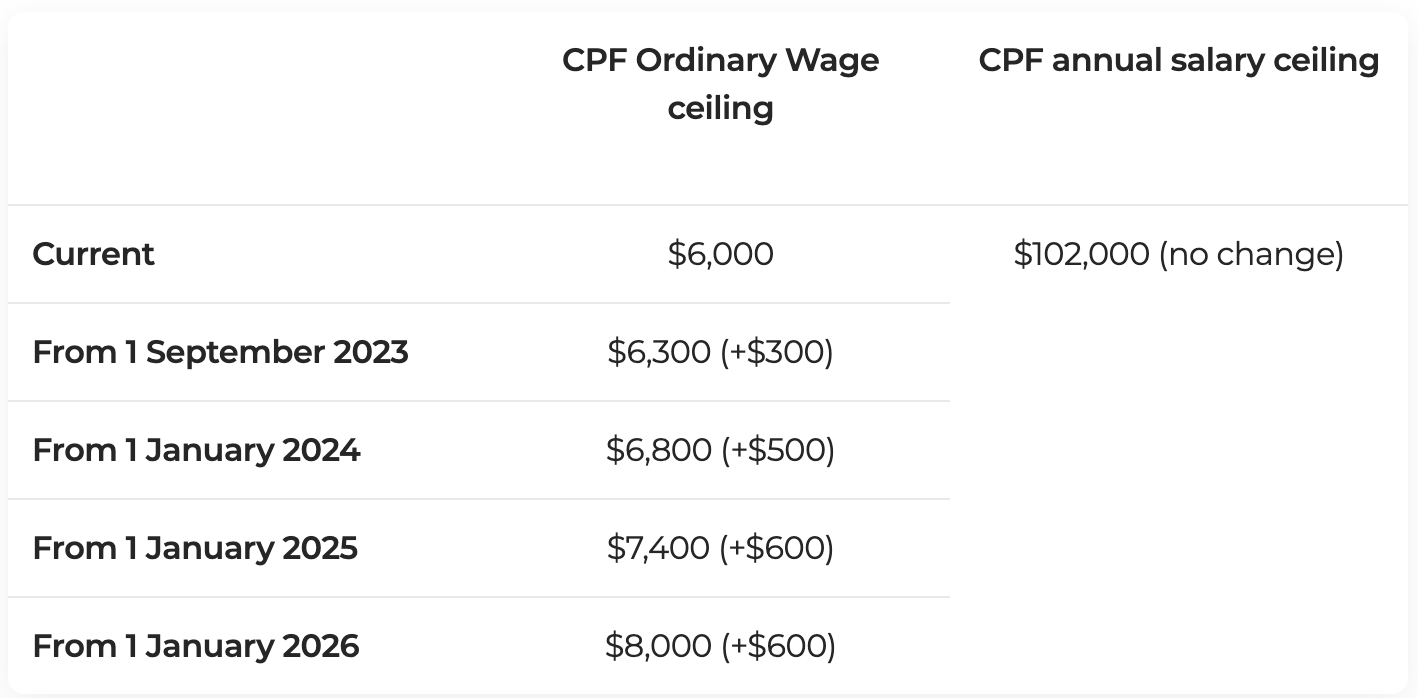

There are limits to how much you can contribute to your CPF accounts each month. This is known as the CPF Wage Ceiling, and comes in two components.

First, the Ordinary Wage Ceiling, which is the gross wage up to which CPF contributions are mandatory. Beyond this ceiling, CPF contributions are not needed.

The Ordinary Wage Ceiling is being progressively raised from S$6,000 prior to September 2023, to S$8,000 by 2026. See the following table.

source: CPF Board

Example: Let’s say your gross salary is S$6,500. In 2024, you and your employer need to contribute CPF based on the entire S$6,500.

Prior to that, in Oct 2023 when the Ordinary Wage Ceiling was S$6,300, you and your employer need only contribute CPF on S$6,300.

Note that ordinary wages in excess of the prevailing Ordinary Wage Ceiling are not subject to CPF contributions. Hence, if you are drawing a gross salary of S$8,000, your take-home salary from 1 January 2024 will be as follows:

- Gross wage: S$8,000

- Ordinary Wage Ceiling (Jan 2024): S$6,800

- No CPF contribution needed: S$1,200

- Take home pay = (0.8 x S$6,800) + S$1,200 = S$6,640

Next, the Additional Wage Ceiling concerns your additional wages, such as bonuses. It is calculated accordingly: S$102,000 (minus) annual ordinary wages subject to CPF for the year. CPF contributions are applied on your total additional wages if they fall below the Additional Wage Ceiling.

Example: Your gross salary is S$7,000. You receive 3 months bonus pay of S$21,000. The Additional Wage Ceiling is S$102,000 - (S$6,500 x 12) = S$24,000.

Your total bonus is S$21,000, below the Additional Wage Ceiling. Hence both you and your employer have to make CPF contributions on the S$21,000.

What is the CPF Annual Limit?

There is a limit to how much money your CPF account can receive each year. This is known as the Annual Limit, and is currently set at S$102,000.

The Annual Limit applies to both mandatory contributions and voluntary contributions (such as cash top-ups to your CPF accounts that you make on your own accord). However, from 1 Jan 2022, it will no longer be applied to the MediSave top-up limit.

The 4 CPF accounts and their uses

A CPF member will have three CPF accounts until age 55, whereupon a fourth account is automatically created. Let’s take a look at what these accounts are and their uses.

| Ordinary Account (OA) | May be used for housing, insurance, investment and education |

| Special Account (SA) | For old age and investment in retirement-related financial products |

| Medisave Account (MA) | For hospitalisation expenses and approved medical insurance |

| Retirement Account (RA) | For retirement needs, Automatically created on your 55th birthday by merging your OA and SA monies |

Ordinary Account

The funds allocated to your Ordinary Account (OA) can be used for four purposes: housing, insurance, investment, and education.

By far, the most common use of the OA among Singaporeans is to pay for housing. The OA may be used for purchases of both HDB public housing and private properties, subject to prevailing rules.

There are some differences when using your OA funds to buy a public flat vs a private property, but the important thing to note here is that OA money used to buy private properties must be paid back into your CPF account when you sell the property.

For HDB properties, this requirement does not apply.

For insurance, the OA is most commonly used to pay premiums for the Dependants Protection Scheme (DPS), which is an affordable term life insurance plan that affords CPF members some basic life protection.

Education is another permissible use of the OA funds.

Members can use their OA to pay for their own, their spouse’s, their children’s or their relative’s subsidised tuition fees for approved courses. The amount used for education must be paid back by the student starting one year from graduation. However, the member may apply to waive the replacement if qualifying conditions have been met.

Lastly, the OA can also be used for investment in various CPFB-approved financial products. Such investments are not guaranteed by the Board, and a member could make a loss on their OA investments. Although the funds in your OA are short-term in nature, always do your due diligence when investing. The money is largely meant for housing and education after all.

Special Account

The Special Account (SA) has a more restricted range of uses compared to the OA, ostensibly because the money in this account is meant to be used to meet retirement needs.

As such, the SA funds can only be invested in a narrower range of financial products, including unit trusts, investment-linked policies, annuities, treasury bills, endowment policies, and Singapore Government Bonds, to name a few. If you’re familiar with financial products, you’ll notice these are commonly considered to be lower-risk investments.

Besides these low-risk investments, there’s not much else you can do with your SA, except topping it up with cash or monies from your OA — a move which is irreversible and irrevocable.

MediSave Account

Like its name suggests, the MediSave Account (MA) is used primarily to cover medical and healthcare needs.

This coverage takes the form of MediShield Life, a national health insurance scheme, which provides a range of benefits to cover basic medical procedures, day surgery and hospitalisation fees and certain outpatient expenses for life.

Premiums for MediShield Life may be fully paid via the MA. Additionally, the deductible, co-insurance and any leftover amount on your hospital bill can be paid using your MA.

If you're confused about the differences between MediSave and MediShield, read this for a 2-minute explainer.

Retirement Account

On your 55th birthday, you will gain a new Retirement Account (RA). This is used to fund your CPF Life payouts; a lifelong annuity scheme designed to assist members in meeting their retirement and old age needs.

It happens this way: At the point your RA is created, whatever funds available in your OA and SA are transferred to your RA. The combined funds then continue to accrue interest in your RA and from age 65 onwards, you begin receiving monthly payouts from your RA. How much you receive each month depends on how much was in your RA at age 65.

Meanwhile, your OA and SA continue to exist and function as per normal, subject to prevailing contribution and allocation rates. money in these accounts may be shunted to the RA, or may be withdrawn by the contributing member upon meeting certain eligibility criteria.

CPF interest rates

Now we come to, perhaps, the most important question you’ve been meaning to ask. How much interest do the CPF accounts — OA, SA, MA and RA — earn?

Well, CPF interest rates are a little bit complicated, so we’ll explain the interest rates for each account in turn. But first, look at the following table, which tells you what the prevailing CPF interest rates are.

| Account | Interest rate (per annum) |

| OA | Up to 3.5% |

| SA | Up to 5% |

| MA | Up to 5% |

| RA | Up to 6% |

Ordinary Account (OA) earns up to 3.5% per annum

Funds in your OA earn up to 3.5% interest per annum, but only on the first S$20,000 in this account. Once your funds accumulate past S$20,000, you’ll earn 2.5% interest per annum instead. If you're wondering why, your OA's funds are short-term in nature, as mentioned above. The money is meant to be used for insurance premiums, a first home purchase, and tertiary education.

The interest rate in the OA is reviewed quarterly, and is legislated to be a minimum of 2.5%, or or the 3-month average of major local banks' interest rates, whichever is higher.

Special Account (SA) and Medisave Account (MA) earn up to 5.08% per annum

Funds in your SA and MA earn up to 5.08% interest per annum, but only if your combined balance is S$60,000 or below (with S$20,000 from the OA). Beyond this, your SA and MA grows at 4.08% per annum.

Savings in your SA and MA are invested in the Special Singapore Government Securities (SSGS), which currently earn either:

- 4.08% per annum, or

- the 12-month average yield of 10-year Singapore Government Securities (10YSGS) plus 1%, whichever is the higher. SA and MA interest rates are adjusted every quarter.

Retirement Account (RA) earns up to 6.08% per annum

Last but not least, your RA, which is created for you when you turn 55, can earn as much as 6% of interest per annum.

Just like the SA and MA, the RA earns either:

- 4.08% per annum, or

- the 12-month average yield of 10-year Singapore Government Securities (10YSGS) plus 1%, whichever is the higher.

The prevailing interest rate of the RA is 4.08% per annum. On top of this, you can get an extra 1% of interest on the first S$60,000 of your combined balance and, if you’re 55 and above, a further 1% interest on the first $30,000 of your combined balance (with S$20,000 from the OA).

The RA interest rates are reviewed annually, so rest assured that they are in line with how well Singapore is performing economically.

*note that the interest rate for the CPF SA, MA, and RA will go up 4.05% p.a. in Q3 2024 (1 July 2024 to 30 September 2024).

In conclusion

CPF might be a complicated - and sometimes touchy - subject, but the social security scheme is one that's vital for every Singaporean and Permanent Resident. Even if you're planning to migrate one day for professional or personal purposes, you still need to make the most out of your CPF monies while you're in Singapore. And your plans might change over time too.

Each of the four CPF accounts and resulting schemes have a purpose, whether for retirement needs or healthcare expenses. It might be a complex plan but it's one that holistically addresses an individual's needs at every life stage.

And if you think you’ve now got an inkling on how CPF really works, read SingSaver's story on how Singapore’s very own Mr. CPF, Loo Cheng Chuan, grew his wealth.

![]()

SingSaver Exclusive Offer: Open a Tiger Brokers account and fund a minimum amount of USD 1,000 within the promotional period to receive S$140 Cash, S$140 Shopee Vouchers, or Apple AirTag (4 pack) (worth S$149). Offer is stackable with Tiger Brokers' welcome offer. Valid till 1 May 2025. T&Cs apply.

Read these next:

CPF Investment Scheme (CPFIS): Guide To Investing With Your CPF

Uniquely Singaporean Things We Do To Accumulate Wealth

Complete Guide To CPF LIFE: Facts, Myths And How To Make It Work Harder

Pros And Cons Of Keeping Your Savings In Your CPF Special Account

CPF Special Account (SA) Shielding: How You Can Perform This Retirement ‘Cheat Code’

Similar articles

Pros And Cons Of Keeping Your Savings In Your CPF Special Account

What Are The Consequences of Dodging CPF Contributions?

The SSB vs CPF: Which One Has Better Returns?

MediSave, CPF OA And CPF SA: How Much Does A Self-Employed Person Need To Contribute?

How To Build Sustainable Retirement Income With Your CPF Money

4 Reasons Why You Should Voluntarily Contribute To Your Children’s CPF

Building A S$100,000 Net Worth By 30: Is It Possible?

CPF Has No Equal as Investment Vehicle: Singapore’s Mr. CPF

Back to Blog

Back to Blog

-2.png?width=280&name=Insurance%20(2)-2.png)